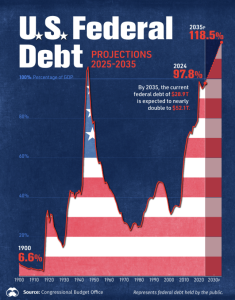

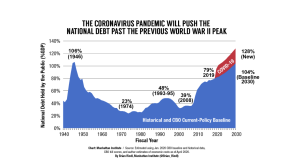

The United States entered the trillions in debt in 1981. The money is owed to a cluster of domestic and foreign creditors, and has been building up over the course of 45 years. Now, The U.S. is in a debt of $39 trillion.

$39 trillion is a baffling number to anybody, even millionaires (or billionaires). It would take 48 Elon Musks in order to pay off the U.S. debt. Not even the richest person in the world could make a miniscule dent in this immense debt. The numbers have been growing higher and higher, and according to Visual Capitalist, are predicted to rise 175% by 2056. The average spectator would wonder how and why our country has raked up this much debt.

What does the U.S. being in “debt” actually entail?

The idea that a country as large and important as the United States could be in debt is difficult to process. How could a country even be in debt? To whom do we owe, and to what extent? The U.S. national debt simply means that our country owes its creditors a certain amount of money, “creditors,” meaning foreign countries (Japan, China, United Kingdom), the federal reserve (U.S. central bank), and domestic private investors (individual U.S. citizens, private banks, mutual funds). The main causes of the federal debt are the imbalance between government spending and tax revenues (basically Social Security, Medicare, and Medicaid), the COVID-19 Pandemic, the Great Recession, and various military conflicts.

How can our government get out of the deep end?

Over the years, and over the course of multiple presidential legislations, the debt has been handled in a number of ways. President Andrew Jackson is famous for being the only president in U.S. history to fully and completely pay off our country’s debt. But how did he do it? According to NPR, Jackson was a proud man, and he considered the U.S. debt to be a “moral failing.” He regularly cut off the building of canals and roads, sold large amounts of land, taxed imported goods further, and dismantled the Central Bank. President Abraham Lincoln introduced the first federal income tax, and President Woodrow Wilson heavily taxed high earners. Along with many other ways of handling this issue, presidents Donald Trump and Joe Biden both handled it in a poor manner — Biden’s administration adding $7 trillion to the national debt and Trump’s administration amassing closer to $8 trillion. These numbers were heavily caused by the COVID-19 pandemic, but they also were affected by the 2017 Tax Cuts and Jobs Act, authorization of substantial spending expansions (defense hikes and veterans’ benefits), and interest costs.

How much are Biden and Trump’s debt growth excused by the severity of the COVID-19 Pandemic?

People such as Senator Rand Paul dedicate their time into calculating the “unnecessary and often absurd government spending.” Dr. Paul states that President Trump, in his first term, spent $400,000 to determine whether lonely rats seek cocaine more than happy rats, $12 million on a pickleball complex in Las Vegas, $2 million to New York University to study kids looking at Facebook ads about food, and “the list goes on and on.” It has been studied, as well, that Biden spent $521 million in grants for EV charging and alternative-fueling infrastructure in 29 states and $30 billion on the electrification of America’s vehicles. So, I do think it is safe to say that while a big chunk of the U.S. debt is due to COVID-19, the unnecessary spending mentioned before contributes to this money-sucking black hole the government seems to be casually throwing its money into.

What are we doing now in order to lessen this debt?

Our current president, Donald Trump, is relying heavily on sweeping tariffs of imported goods, but he is also attempting to restrict improper government payments (which is ironic, considering the ridiculous expenses mentioned before) and implementing strict cuts on discretionary spending. Trump’s “One Big Beautiful Bill” introduces a strategy passed by congress on July 4, 2025.

The bill restricts spending, extends tax cuts, and reduces federal spending on healthcare, student loans, and food assistance. (For example, no tax on spending, $6,000 senior deduction, no tax on tips). But how much will this bill cost the United States over the years?

According to the Bipartisan Policy Center, the OBBB will cost $3.4 trillion over the next 10 years and more than $4 trillion when accounting for additional interest owed on the national debt. So, the question lies in a moral and economic gray area. While the OBBB helps citizens, the requirements for this bill to include you are specific: it includes certain groups such as senior citizens, workers, and families, but provides disadvantages to immigrants, cuts Medicaid by a substantial amount, and tightens work requirements for SNAP recipients (which is estimated to cut food assistance for about 4 million people). The One Big Beautiful Bill also completely ends the Grad PLUS loan program, and caps unsubsided loans at $20,500 and $100,000 lifetime. While this bill has its upsides for citizens, some groups are heavily affected by it, and it is also predicted to add a substantial amount of money to the U.S. national debt.

Should we, as U.S. citizens, be worried about it?

The United States national debt does not pose a certain and immediate economic collapse, but if you care at all about your money and the economy, it is something to keep your eye on. The U.S. debt has been a major long-term concern, and it will most likely continue to be in the future.

The United States national debt does not pose a certain and immediate economic collapse, but if you care at all about your money and the economy, it is something to keep your eye on. The U.S. debt has been a major long-term concern, and it will most likely continue to be in the future.

The most you can do is educate yourself and fact check. Do not donate to the Venmo or Paypal the treasury department has opened. So, while this debt may not affect you directly, being aware of where it is heading is very important as a citizen. It might begin to affect you directly in the coming years, and the best you can do for yourself is be knowledgeable.